July 24, 2018

Appraisals are necessary for any type of loan, because after all, lenders need to know that they can get their money back if someone defaults on their payments!

Without an appraisal, a lender would not know if the item was worth the amount that a person wanted to take out a loan for, and while that could be bad for the lender, it can also be bad for the borrower when they go to sell in the future.

When a person is having new home construction completed, creating an appraisal can be quite tricky, because there is nothing to look at yet. Therefore, in these types of situations, lenders find themselves creating subject to value appraisals. With these types of appraisals, the loans are contingent on the finished home matching what was provided on paper in the beginning.

Every subject to value appraisal report must include three sections including:

-

Where the property is located and general information about the property

-

How much everything will cost including the cost of the lot, the cost of constructing the main structure, and the cost of constructing the out buildings

-

What the cost comparison is for similar sales in the area

The first section always includes important information about zoning and available utilities. This section is necessary, because it will list whether or not a person is trying to do new home construction within a residential or non-residential zone. Some lenders will only approve a loan within residential zoning, while others are a little more lenient if the majority of the properties in the area are residential.

The second section includes the cost of constructing and purchasing everything and how it relates to what it would cost to replace everything. The total of each individual line item must equal the replacement cost analysis or be within the fifteen percent variable. Anything above the fifteen percent requires a detailed written explanation as to what happened to create the difference.

The cost comparison that is completed in the third section will ensure that the new home construction is in line with other homes in the same area. Most of the time, the cost comparisons are done within a five-mile radius, although this could be slightly different depending on where the house is going to be built. The prices of the comparable homes in the area should match up with the cost of the home that is being constructed. If it doesn’t, then a red flag may come up as to why the prices are not the same and the loan may not be approved unless some changes are made.

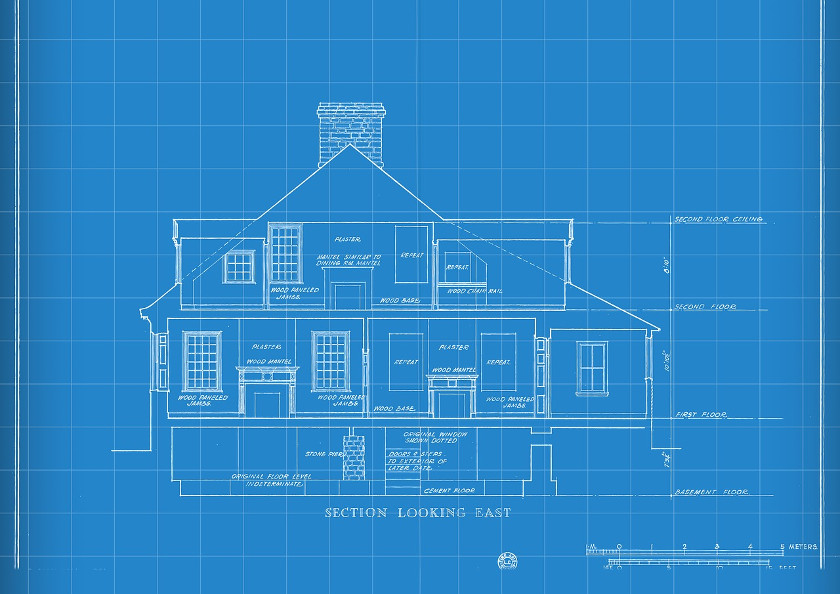

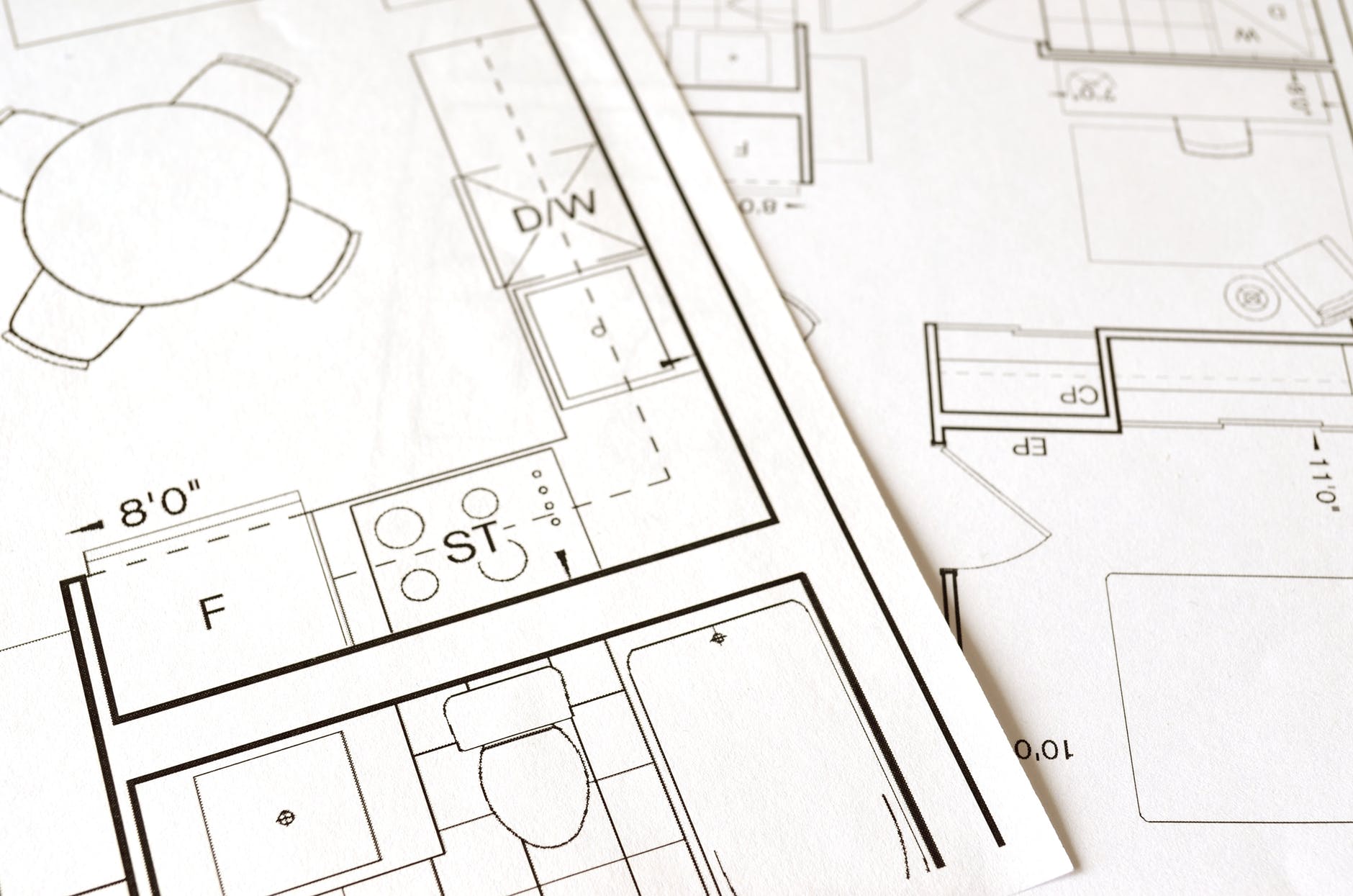

When a lender is completing the subject to value appraisal, it is helpful that they have certain items from the contractor. The first thing that contractors need to give to the lender are the building plans, as they will show the complete design of the home. The floor plan will show all the dimensions, as well as where the electrical and mechanical items will be placed. The spec sheet should be attached to the building plans and each material that is going to be used should be listed on that. This includes the materials for both the inside and the outside of the home.

A plot plan should also be given to the lender from the contractor, as it will show what the property surrounding the home looks like. This plan includes any septic systems, wells, the drainage, utility lines, and more. It can be helpful for lenders to be aware of these items as they can raise or lower the value of a home.

Since the contractor knows what materials will be used, he will be able to create the cost breakdown for each one as well as the labor that is needed for the entire project. This document is the most helpful one for lenders, as it can help determine the value of the home.

The more that is given to the lender, the better chance that the subject to value appraisal will be accurate in both the beginning and end stages of construction.

Construction loans and mortgage loans all utilize the same standardized appraisal report, however, construction loans are always prepared with “Subject To” instead of the “As Is” of the mortgage loans. The construction loans are always subject to the plans and permits, and how the home looks at the end of the construction process.